An electric fleet is fast becoming normal. According to the Society of Motor Manufacturers and Traders (SMMT), electric vehicles (EVs) now account for over 75% of new corporate car registrations in the UK, and it’s easy to see why:

| Diesel |

Electric |

|

| BiK Tax Rate | 15%- 27% | 4% |

| Cost per mile | 13p-15p |

2p-4p |

| Annual maintenance costs | £400-£800 | £150-£300 |

Surging costs of ownership are the number one concern for fleet owners. EVs can cut these at a stroke, so it’s understandable why so many of our fleet insurance customers have made the transition.

There is a downside, however. Electric commercial vehicles introduce new operational and insurance exposures that many businesses do not fully understand until they come to make a claim. This is why insuring an EV fleet typically costs 10% to 25% more on average than insuring a diesel fleet. To our customers, that means around £125 more per vehicle.

As the owners of the UK’s leading independent fleet insurance broker, I thought these risks needed to be explained. In this guide, I’ll look at the insurance risks associated with EV fleets, including battery damage, charging liability, repair delays, and vehicle weight issues. I’ll also give you tips on reducing these risks and getting cheaper fleet insurance quotes.

I hope this guide will prove useful, but if you’d like some help or an insurance quote, please get in touch. You can call us on 01482 434343, request a callback, or get a fleet insurance quote.

Andy

Why Electric Fleet Insurance Is Different

Electric vehicles are not simply petrol or diesel vehicles with batteries added. They introduce entirely new risk profiles for insurers. Traditional fleet insurance models are built around internal combustion engine vehicles, technology that insurers have decades of experience with. EV is new, and there are plenty of unknowns:

- Vehicle values and depreciation

- Repair costs

- Fire risks

- Breakdown exposure

- Theft trends

- Driver behaviour

- Downtime duration

- Third-party claim costs

- Environmental and road damage

Insurance underwriters hate unknowns. This means that for businesses operating multiple EVs, changes can have a significant financial impact.

Battery Damage Is One of the Biggest Risks

A fleet customer of mine told me that his leasing company advised him against leasing his electric cars for more than three years. ‘You’d be mad to. We simply don’t know what’s going to happen with the batteries.’

This speaks volumes for EVs.

The battery is the most expensive component in an electric vehicle. In some commercial EVs, the battery can account for 40% of the vehicle’s total value. If they’re damaged, then the vehicle is almost certainly going to be written off, a situation that worries insurers.

Why Battery Claims Are Complicated

The cost of repairing a diesel car after an accident ranges from £500 to £5,100 according to the RAC Foundation. Minor collision repairs range from £1,000 to £3,500, while significant structural or battery damage can escalate repair bills to £10,000 or more. EV repair costs are 30%-50% higher overall, as even a minor impact can damage:

- Battery cells

- Cooling systems

- Protective casings

- Electrical wiring

A low-speed accident that would be repairable on a diesel is likely to be a write-off on an EV.

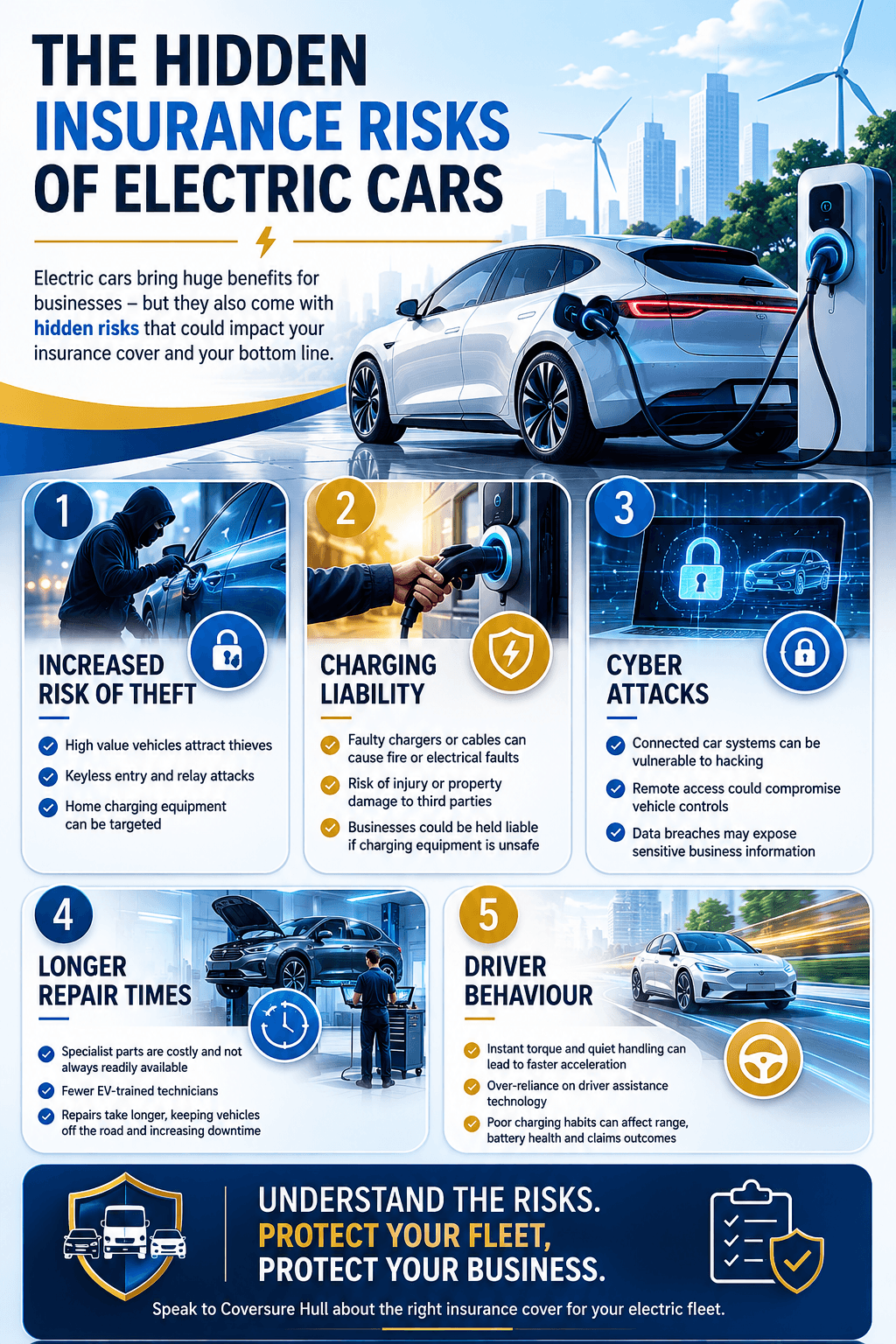

EV Repairs Often Take Much Longer

One of the hidden operational risks of electric fleets is repair downtime. Many garages still lack:

- EV-certified technicians

- Specialist battery equipment

- Safe repair facilities

- Manufacturer-approved repair capability

This can lead to:

- Longer repair queues

- Delayed parts availability

- Extended vehicle off-road periods

For fleet operators, downtime is often more expensive than the repair itself. This is compounded by the need for insurers to provide replacement vehicles, which forces premiums up.

The Business Impact of EV Downtime For Fleets

A fleet that’s off the road costs money. Longer repair periods result in:

- Missed appointments

- Lost contracts

- Customer dissatisfaction

- Service level agreement penalties

Many of my truck and HGV insurance clients have cited concerns over downtime when we’ve discussed transitioning to EV. While their main concerns are range, cost of vehicles, lack of models, and charging restrictions, downtime is a massive issue. When your fleet is your business, disruption can be fatal.

Charging Infrastructure Creates New Liability Risks

No business owner would be without liability insurance, but most overlook the liability implications of charging infrastructure. With private charging costs as little as a tenth of the cost of public ones, 7p to 30p per kWh against 54p to 85p per kWh, it’s easy to see why fleet owners are installing them. But commercial charging points introduce several potential liabilities:

- Fire Risks – although EV fires remain rare, lithium-ion battery fires are difficult to extinguish and can cause extensive damage. A diesel or petrol vehicle fire typically reaches temperatures between 800°C and 1,000°C; a lithium-ion battery fire can reach 1,200°C to over 2,700°C, which is the same temperature as an oxy-acetylene welder.

Battery fires could be caused by:

- Faulty charging equipment

- Damaged batteries

- Electrical faults

- Overheating

- Poor installation

A charging-related fire at a depot could damage:

- Buildings

- Stock

- Neighbouring vehicles

- Equipment

- Employee’s property

Fire crews need specialist equipment to deal with these fires and huge volumes of water. So, depending on your location, these could take time to arrive, which increases the risk of damage and injury.

Public Liability Risks From Charging Equipment

Charging cables and charging stations can also create public liability exposure, such as:

- Trip hazards

- Cable obstruction injuries

- Damage caused by faulty chargers

- Third-party vehicle damage

Businesses installing workplace chargers should ensure their liability insurance reflects these new risks.

Electric Vehicles Are Heavier Than Diesel Ones

Battery packs add substantial weight to electric vehicles. This additional weight raises issues over:

- Safety issues

- Braking problems

- Tyre wear

- Suspension damage

- Increased accident risk (owing to slower braking)

From a commercial vehicle insurance perspective, overloaded vehicles may:

- Invalidate policy conditions

- Increase liability exposure

- Affect claims outcomes

This is particularly important for:

- Courier fleets

- Construction fleets

- Tool-carrying trades

- Refrigerated transport businesses

Fleet operators should review payload management when transitioning to EVs. We have a courier client who transitioned, and her new EV van exceeded the 3.5 tonne limit. We spotted this and advised her to get truck insurance instead. Without this, she’d have had an invalid policy, and her business would have been operating illegally.

Water Damage Risks Are Increasing

Extreme weather and flooding continue to affect businesses across the UK. Electric vehicles contain high-voltage systems that can be vulnerable to water exposure. Water-damaged EVs are extremely expensive to repair, assuming it can be done at all. If water reaches critical battery components, insurers may consider the vehicle unsafe to repair, meaning:

- Vehicles being written off

- Battery contamination

- Electrical system failure

- Fire risk after recovery

Businesses operating in flood-prone areas should review:

- Overnight parking locations

- Depot drainage

- Route planning

- Severe weather procedures

UK Centre for Ecology & Hydrology (UKCEH) figures suggest that 1 in 6 properties in the UK are at risk of flooding. The Environment Agency says that in England alone, 6.5 million properties are at risk, and that by 2050 the figure will be over 8 million.

EV Thefts Are Rising

Reported thefts rose by 8% in 2025. While this is largely due to there being more of them to steal, thefts are rising thanks to new techniques. Relay attack, using relay devices to capture and amplify your key fob’s signal, tricking your car into unlocking without the actual key present, and Onboard Diagnostic (OBD) hacks, where criminals plug in a device that programs a new key. Other common EV theft risks include:

- Charging cable theft

- Keyless vehicle theft

- Organised vehicle theft

- Battery component theft

Some electric vans also contain valuable onboard technology systems that increase their attractiveness to thieves. Fleet security remains essential if you want to keep premiums down.

Cyber Risks and Connected Vehicle Technology

Modern electric fleets rely heavily on software and connectivity, and this leaves them open to cyber-attacks as many vehicles now feature:

- GPS tracking

- App-based controls

- Remote diagnostics

- Telematics

- Over-the-air software updates

- Signal relays for unlocking vehicles

Potential risks include:

- Vehicle hacking

- Data breaches

- GPS interference

- Remote immobilisation

- Software failures

As connected fleet technology expands, insurers are increasingly considering cyber resilience during underwriting. Cyber-attacks of all kinds are a huge concern to insurers, but the rise in in-car attacks has been frightening. Signal relay accounts for 58% of all vehicle thefts in the UK, according to the police, and in-car systems are being used to access other data and plant ransomware.

The problem has become so severe that insurers, including Munich Re, Axa, and Zurich, are offering cyber insurance cover as part of their fleet policies. This, of course, comes at a price.

Breakdown Recovery for EVs Is More Complex

Recovering a broken-down electric vehicle isn’t always straightforward. Some EVs cannot be towed conventionally because regenerative braking systems may be damaged. Specialist recovery procedures may be required, which add costs to the insurer and ultimately the policyholder. Recovery often also takes longer, which adds other costs:

- Longer roadside delays

- Limited recovery availability

- Higher recovery charges

- Additional transport costs

Driver Training Is More Important Than Ever

Many businesses underestimate how differently electric vehicles behave compared to diesel vehicles. Put your foot down in an electric car, and you’ll experience extraordinary acceleration. This is due to the delivery of instant torque, something that doesn’t occur in internal combustion engines. Without proper training, drivers may:

- Misuse of regenerative braking

- Drain batteries inefficiently

- Overload vehicles

- Damage charging equipment

- Increase accident exposure

Insurers care about training as it shows fleet owners take risk management seriously. Many now assess:

- Fleet owners’ EV driver training programmes

- Telematics usage – as it shows how EVs are being driven

- Charging policies

- Fleet safety procedures

Businesses with strong risk management may achieve:

- Cheaper cover

- Fewer claims

- Reduced excesses

Battery Degradation Can Affect Fleet Value

Residual value uncertainty remains a concern for many insurers and fleet operators. While 75% of fleets lease rather than buy their vehicles, concerns over battery degradation still matter to insurers, as it can affect:

- Vehicle valuations

- Total loss settlements

- Lease agreements

- Resale values

If fleet operators can show they are monitoring battery health carefully, they can get better terms with insurance providers.

The EV Insurance Market Is Still Evolving

Electric fleet underwriting remains relatively new. As insurers collect more claims data, so underwriting appetites and pricing will continue to change. In the short term, this means businesses are likely to experience:

- Fluctuating premiums

- Changing policy conditions

- Stricter risk requirements

- Evolving (stricter) security expectations

Fleet operators need to review their insurance regularly to ensure cover keeps pace with operational changes.

How Businesses Can Reduce Electric Fleet Insurance Risks

The good news is that many EV-related risks can be managed effectively with the right planning. Demonstrate these to your insurer, and premiums can tumble. Invest in driver training on:

- Efficient driving

- Charging procedures – to avoid public liability claims

- Payload awareness

- Emergency response procedures

Use telematics to monitor:

- Driving behaviour

- Harsh braking – a major problem for EVs

- Battery use optimisation – through careful driving

- Route efficiency

Improve fleet security:

- Vehicle trackers

- Immobilisers

- Secure depot parking

- CCTV

- Charging point security

Review charging infrastructure and ensure they are:

- Regularly inspected

- Safely positioned

- Appropriately maintained

Plan for downtime and develop contingency plans for:

- Longer repair periods

- Replacement vehicle shortages

- Charging failures

Electric Fleets Still Offer Major Long-Term Benefits

Despite the risks and potential increase in fleet insurance quotes, electric fleets are the future of fleets, and EV fleet owners will see:

- Lower tax burdens

- Lower congestion charging fees

- Lower fuel costs

- Reduced emissions

- Improved brand reputation

- Lower maintenance costs

- Compliance with environmental regulations

However, successful EV adoption requires more than simply replacing diesel vehicles with electric alternatives. Fleet operators must understand how insurance risks are changing alongside vehicle technology.

Final Thoughts

Electric vehicles are bringing huge benefits to the fleet sector, but they’re bringing hidden insurance challenges. Battery exposure, charging liability, repair delays, cyber risks and evolving underwriting standards all create new considerations for fleet managers. Businesses that proactively manage these risks are far more likely to:

- Reduce claims

- Get cheaper fleet insurance quotes

- Minimise downtime

- Protect operational continuity

- See fewer accidents

As electric vehicle technology continues to evolve, fleet insurance will evolve with it. Understanding these changes early can help businesses make smarter decisions and avoid costly surprises in the future.

Like Some More EV Fleet Insurance Help?

If you’d like some help or an insurance quote, then please get in touch. You can call us on 01482 434343, request a callback, or get a fleet insurance quote.

About The Author

Andy Price Dip. CII is the founder and Managing Director of Coversure Hull, Coversure North Lincs, Coversure Peterborough, and Coversure Online. He holds a Diploma in Insurance and has over 30 years of fleet insurance experience.